Inventory Accounting Methods:

FIFO and LIFO Accounting,

Weighted Average Cost

Previous lesson: What is Inventory?

Next lesson: Sales, Cost of Goods Sold, Gross Profit

The FIFO and LIFO accounting methods as well as the Weighted Average Cost method are three methods used when accounting for inventory.

As you'll see below, each of these three methods result in different values for your inventory at the end of the accounting period as well as your cost of goods sold.

In this lesson we're going to look at all three methods with examples.

Be sure to check your understanding of this lesson by taking the quiz in the Test Yourself! section further below. And right at the bottom of the page, plenty more questions on the topic submitted by fellow students.

Inventory Valuation and Tracking

Businesses need to keep track of which items they sell and which items they have on hand, including their exact value.

During the year your inventory on hand is valued at how much it cost you to buy it (or if you're a manufacturing business - to make it). Each time you receive inventory you simply record how much it cost and enter it in your accounting system.

Now, there are two broad categories of accounting systems for inventory - you can use the periodic or perpetual system to track your inventory.

With the perpetual system, you keep perpetual (constant) track of how much inventory you have on hand and exactly how much they're worth. This is the case with computerized systems, systems involving barcode scanning, etc.

With the periodic system of accounting one knows how many goods and what their values are only at certain points in time. One does not keep constant track of them. This is the case where one just keeps simple inventory records and does a periodic (occasional) physical stock count.

Check out our lesson on the periodic or perpetual system of inventory for more detailed explanations and examples of these systems.

When using the periodic system, at the end of each period (month or year) one should always do a physical inventory count to determine the number of inventory on hand (actually, this should also be done for a perpetual system - in this case to just confirm the quantity of inventory shown on your computerized inventory system).

With a perpetual inventory system you'll be able to tell the value of the goods on hand by simply getting this data from your computerized accounting system.

But with a periodic system, you need to actually place a value on the goods you have in stock.

One would think this would be easy - the value of the goods is simply how much they originally cost. Unfortunately there is a bit more to it than just this.

For example, how do you know that the goods you have on hand on the 31st of December are the ones you bought in October, or the ones you bought in September, or the ones you bought earlier in the year?

What happens if all your inventory looks the same, but they cost different amounts at different points in the year? How do you know which ones you sold, and which ones you have on hand right now?

There are three inventory accounting methods used to calculate the value of the goods you have on hand at the end of the period as well as the cost of the goods that you sold.

An Example to Illustrate the Three Inventory Accounting Methods

The following example will illustrate these three methods:

Cindy Sheppard runs a candy shop. She enters into the following transactions during July:

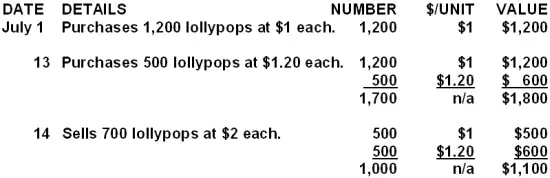

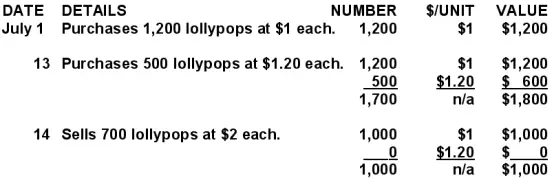

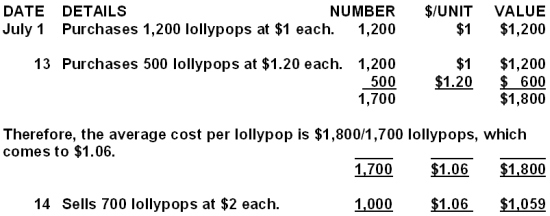

July 1 Purchases 1,200 lollypops at $1 each.

July 13 Purchases 500 lollypops at $1.20 each.

July 14 Sells 700 lollypops at $2 each.

First of all, how many lollypops does she have at the end of the month?

Answer:

1,200 + 500 – 700 = 1,000 lollypops

Now, there are three ways that Ms. Sheppard could value her closing stock:

1. The FIFO Method

The FIFO method is the first option for valuing stock and probably the most common.

What Does FIFO Stand For?

FIFO stands for First In First Out.

What Does FIFO Mean for Valuing Inventory?

The FIFO method assumes that the first inventories bought are the first ones to be sold, and that inventories bought later are sold later.

Applying the FIFO Method to Our Example

Using our example above and the FIFO method, the value of our closing inventories would be calculated as follows:

Using the First-In-First-Out method, our closing inventory comes to $1,100.

This equates to a cost of $1.10 per lollypop ($1,100/1,000 lollypops).

Where Do We Normally Find the FIFO Method Used?

It is very common to use the FIFO method if one trades in foodstuffs and other goods that have a limited shelf life, because the oldest goods need to be sold before they pass their sell-by date.

Thus the first-in-first-out method is probably the most commonly-used method for small businesses.

2. The LIFO Method

Another method that is used, and the opposite of the FIFO method, is LIFO.

What Does LIFO Stand For?

LIFO stands for Last In, First Out.

What Does LIFO Mean for Valuing Inventory?

The LIFO method assumes that the last inventories bought (the most recent) are the first ones to be sold, and that inventories bought first (the oldest ones) are sold last.

Applying the LIFO Method

The value of our closing inventories from our example would be calculated as follows using the LIFO method:

Using the Last-In-First-Out method, our closing inventory comes to $1,000.

This equates to a cost of $1.00 per lollypop ($1,000/1,000 lollypops).

Where is the LIFO Method Used?

The LIFO method is commonly used in the USA.

It is generally not used outside the US.

3. The Weighted Average Cost Method

The weighted average method is a final option for valuing our inventory.

What Does the Weighted Average Method Mean for Valuing Inventory?

This method assumes that we sell all our inventories simultaneously.

The weighted average method specifically involves working out an average cost per unit at each point in time after a purchase.

Applying the Weighted Average Method

Using the example above, the value of our closing inventories would be calculated as follows:

Using the weighted average cost method, our closing inventory amounts to $1,059.

This equates to a cost of $1.06 per lollypop ($1,059/1,000 lollypops).

Where is the Weighted Average Method Used?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

The weighted average cost method is most commonly used in manufacturing businesses where inventories are piled or mixed together and cannot be separated or differentiated from each other, such as with chemicals or oils.

For example, chemicals bought two months ago cannot be differentiated from those bought yesterday, as they are all mixed together.

So we just work out a weighted average cost for all the chemicals we have in our possession.

FIFO vs LIFO vs Weighted Average Around the World

Generally accepted accounting principles in the United States allow for the use of all three inventory methods.

However, the LIFO method is disallowed in non-US countries (it is disallowed under International Financial Reporting Standards, which are the accounting standards most of the world uses).

The FIFO method and the weighted average cost method are used in non-US countries.

In recent years there have been calls for the standardization of accounting rules throughout the world and there has been talk specifically about disallowing LIFO in the US (or making the rest of the world follow the LIFO system, which is probably unlikely to occur).

Anyway, as of this writing the matter has not yet been resolved and so the differences in inventory valuation still exist.

Test Yourself!

Before you start, I would recommend to time yourself to make sure that you not only get the questions right but are completing them at the right speed.

Difficulty Rating:

Intermediate

Quiz length:

7 questions

Time limit:

8 minutes

Important: The solution sheet on the following page only shows the solutions and not whether you got each of the questions right or wrong. So before you start, get yourself a piece of paper and a pen to write down your answers. Once you're done with the quiz and writing down your answers, click the Check Your Answers button at the bottom and you'll be taken to our page of solutions.

Good luck!

Well, that's it for our lesson on FIFO and LIFO accounting and the weighted average method. We hope these inventory accounting methods are a bit clearer now!

In our next lesson we're going to take a look at Cost of Goods Sold, the key expense for businesses that have inventory, and we'll see how FIFO, LIFO and the average method affect the cost of goods sold expense and the profit figures for a trading business.

We'll also look at the cost of goods sold formula, an equation which has left many an accounting student and practitioner somewhat confused, or at a minimum, having to resort to outright parroting. Our simple explanations of this formula should make it much easier to remember.

So if you're good with this lesson, go ahead and head on to our next inventory lesson on Sales, Cost of Goods Sold and Gross Profit.

Stay up to date with ABfS!

Follow us on Facebook:

Previous lesson: What is Inventory?

Next lesson: Cost of Goods Sold

Questions Relating to This Lesson

Click below to see questions and exercises on this same topic from other visitors to this page... (if there is no published solution to the question/exercise, then try and solve it yourself)

lifo and average costing

Under what conditions lifo and weighted average process costing consistently produce same costing figure?

Examples of FIFO Products in Real Life

Q: Give at least 5 examples of fifo in general life?

A: There are many real-life examples of products that are more suited for a FIFO (First-In-First-Out) …

FIFO Method Question

Date Particulars Units Rate

01.03.09 opening stock 100 $1.75

05.03.09 purchased 150 $1.50

12.03.09 …

What is the Best Inventory System: Perpetual or Periodic?

What is the best inventory method that can be used in an organization?

Weighted Average Cost Question

(Multiple Choice)

If the company uses weighted average method for inventory valuation, the value of inventory as on March 31, 2005 is:

a. $11967

b. $12000

c. $12500

…

Inventory Ledger Account Exercise

Below is the records of receipts and issues of a certain material in a factory for the month ending 30th September, 2008.

Receipts:

Sept. 1- opening …

Stock Returns (Weighted Average Cost Method)

What happens when stock is returned, using the weighted average cost method?

Define Reorder Level

What is the reorder level?

Weighted Average Method

Q: What are the advantages and disadvantages of using the weighted average method?

Accounting Question - LIFO Method

Why would tax accountants prefer to use last-in-first-out method?

Pricing System - FIFO, LIFO and Weighted AVerage

There was an opening balance of 100 units which had a value of #3900. Bought: may 100units @ #41, june 200units @ #50, august 400units @ #51.875, sold: …

FIFO METHOD Formula

Q: WHAT IS THE FORMULA FOR FIFO METHOD WHEN CALCULATING THE VALUE OF THE CLOSING INVENTORY?

A: The answer to this question has been brilliantly answered …

Material Pricing and Valuation of Stock

(FIFO, LIFO & Weighted Average Cost Question)

The following details are extracted from the stores ledger card of a small manufacturing company during the month of November 2009 (please note that Shs …

The Weighted Average Cost Method

Q: How do I find the average cost per unit of inventory using the weighted average cost method?

Valuation of Work In Progress under Process Costing

Q: Under process costing, how do you find the cost per unit while using the FIFO method and the WAM method?

FIFO, LIFO & Weighted Average

Cost Exercise

Q: Using FIFO, LIFO, and weighted average, what is the ending cost of inventory?

How are LIFO

Purchase Returns Handled?

Q: How are LIFO Purchase returns handled?

FIFO Method Question

1/3/2009

1 Mar opening balance 880 @ $9

2 Mar purchase 300 @ $6

4 Mar sell 400

6 Mar sell 600

10 Mar purchase 400 @ $8

15 Mar purchase 500 @ $5 …

Weighted Average Cost Per Unit

Q: Dear Sir,

A container of goods has different quantities with different values per unit. For example the total value of the goods are USD 280,000, …

Regarding Valuation of Closing Stock of Raw Materials

Q: I want to know whether storage costs (rent for storage of materials until it is used in production) will be considered for valuation of closing stock …

Advantages of FIFO and LIFO Methods

Q: What are the advantages of FIFO and LIFO methods?

A: FIFO and LIFO are two of the most common inventory accounting methods in use today.

…

Sales Return Under the LIFO Method

Q: What will the entry be if there is a sales return under the LIFO method?

© Copyright 2009-2023 Michael Celender. All Rights Reserved.

Click here for Privacy Policy.

Search this site:

Stay up to date with ABfS!

Follow us on Facebook:

All the lessons on this site and much, much more...

Available Now On

Comments

Have your say about what you just read! Leave me a comment in the box below.